Strong container throughput restricts downturn in an eventful first quarter

- Oprac. M.K.

- Kategoria: English zone

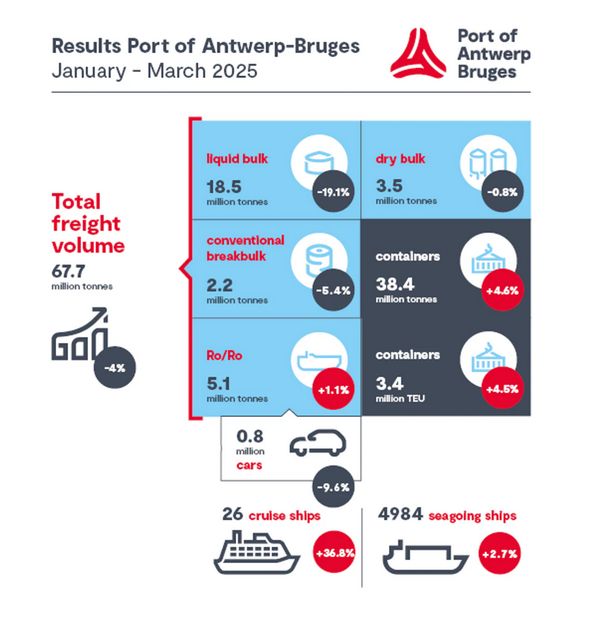

In the first quarter of 2025, Port of Antwerp-Bruges handled 67.7 million tonnes of cargo, a drop of 4.0% compared to the same period last year. This decline was largely driven by a sharp decrease in bulk volumes, while container throughput recorded growth. The port continues to navigate global challenges such as shifting market dynamics, geopolitical tensions and the ongoing pressure on the European chemicals sector. With the United States as its second-largest trading partner, Port of Antwerp-Bruges is closely watching the evolving trade environment, as future tariff impacts become more pronounced.

Container throughput is strong and bulk flows are volatile

Container throughput served as a key growth engine in the first quarter, rising 4.6% in tonnage and 4.5% in TEUs compared to the same period in 2024, despite geopolitical uncertainties and container alliance restructuring. The transition to the new alliances and strikes and congestion at other ports did, however, result in longer container dwell times and therefore put increased pressure on terminal capacity. Port of Antwerp-Bruges' market share in the Hamburg-Le Havre Range increased to 30.5% in 2024, and on a global level, the port climbed from 15th to 14th place in the ranking of the largest container ports.

Liquid bulk saw the steepest decline (-19.1%), with sharp declines in gasoline, naphtha and LNG. Contributing factors included changed market conditions in Africa, reduced naphtha demand from the petrochemicals industry and EU sanctions on Russian LNG transshipment. The throughput of chemicals increased by 10.9%, mainly thanks to a significant increase in biofuels (+128%) Without that boost, the chemical segment would have seen a slight year-on-year drop (-1.7%). Europe’s chemical industry remains under considerable pressure in terms of global competitiveness.

In other segments, the impact of challenging market conditions remained limited. For example, conventional general cargo experienced a modest decline (-5.4%) due to lower iron and steel throughput (-14.3%) as a result of the weak economic climate and import quotas. RoRo throughput rose slightly (+1.1%), even with a sharp decline in new car throughput (-11.3%), which is a reflection of the difficult situation in the European automotive industry. The decline in vehicle throughput was offset by increases in other RoRo cargoes such as unaccompanied freight. Dry bulk remained almost stable (-0.8%).

The impact of U.S. import tariffs remains limited for now

The impact of U.S. import tariffs remains limited for now

The impact of U.S. import duties on traffic in Port of Antwerp-Bruges remains limited for now. Although some companies are acting in anticipation of tariffs, no clear export acceleration toward the U.S. has been noticeable so far. Container exports rose by 3.2%, steel saw a temporary peak in January, and 20% fewer cars were exported to the US, in line with the overall decline in car exports. At the same time, structural factors, such as disrupted shipping schedules in containerised liner trade, model changes on the car market and temporary production suspensions, put increased pressure on terminals. So while the immediate impact remains limited for now, it is clear that further developments in the area of trade tariffs could have an effect on the logistics chain in the coming months.

Structural challenges call for cooperation

In addition to trade tensions with the United States, the European economy, and the industrial sector in particular, is struggling with structural problems that are seriously undermining its competitiveness. High energy and production costs, global overcapacity and increasing competition from cheap imports from Asia and elsewhere are putting pressure on the sector. On top of that, complex regulations, slow permitting processes and high labour costs are interfering with the willingness to invest. In recent years, the combination of these factors led to a sharp decline in market share, added value and production capacity. Port of Antwerp-Bruges and Port of Rotterdam are therefore pleading for a rapid implementation of the Clean Industrial Deal, in the form of concrete measures and sufficient budgetary support to restore resilience and future prospects for European industry.

On top of that, the logistics chain remains vulnerable. The pilots' strike on 31 March temporarily shut down access to the port, resulting in millions of euros in economic damage and a visible impact on the operation and image of Port of Antwerp-Bruges. This disruption affected multiple links in the chain – from shipping companies and terminals to industry and transportation. With another national strike planned to take place on 29 April, uncertainty remains high. The structural challenges, combined with mounting trade pressures with the United States, underscore the need for dialogue and cooperation.